Stablecoins: Bridging the digital divide

A guide for financial professionals

Introduction: The new digital frontier

Stablecoins, once confined to the periphery of the crypto ecosystem, have evolved into sophisticated financial tools and a serious contender for global payment infrastructure. Their rapid ascent, with market capitalization growing tremendously and transaction volumes rivaling traditional payment networks, demands attention from every financial professional, regardless of prior crypto experience. They are viewed as a possible breakthrough innovation in the future of payments.

This post will demystify stablecoins, explaining their foundational characteristics, exploring their powerful use cases, analyzing the critical risks they introduce, and detailing the potential systemic implications for the traditional financial system, particularly the banking sector.

1. Stablecoins 101: Stability meets programmability

Stablecoins are a class of crypto assets designed to combine the transactional efficiency and programmability of blockchain technology with the price stability of traditional financial instruments. Unlike volatile cryptocurrencies such as Bitcoin, stablecoins peg their value to an external reference, typically the U.S. dollar.

1.1. Key characteristics

Stablecoins differ from traditional digital money like bank deposits in two primary ways:

1. Cryptographic security: They are cryptographically secured, allowing users to settle transactions near-instantaneously (often 24/7/365) without relying on a centralized intermediary to validate and prevent double-spending.

2. Programmability and composability: They are built on Distributed Ledger Technology (DLT) standards that are programmable. This “composability” allows them to interoperate with smart contracts (self-executing programmable contracts) to create complex financial services. This feature enables novel applications like automated payments and milestone-triggered disbursements.

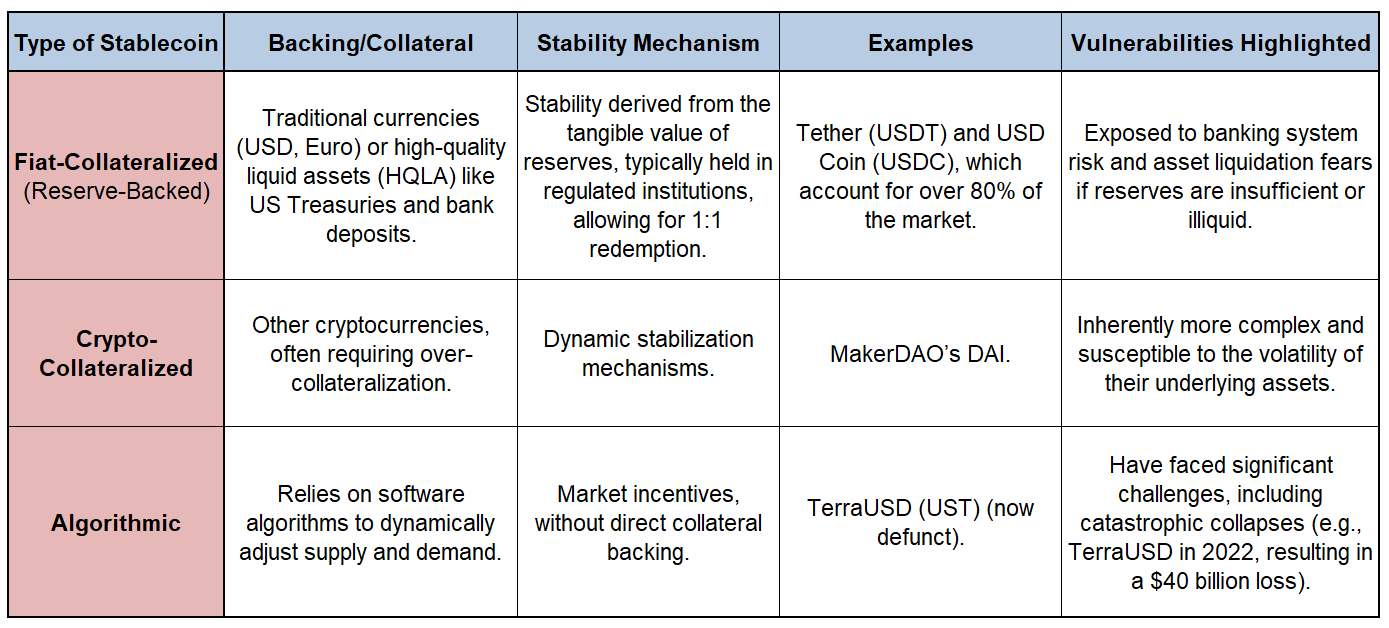

1.2. Types and stability mechanisms

Stablecoins are classified into three primary types based on their stabilization mechanisms and collateral:

2. The killer use cases: Why finance professionals should care

The growth of stablecoins is driven by robust, real-world use cases that address significant inefficiencies in current financial infrastructure.

2.1. Cross-border payments and remittances

Stablecoins offer a compelling solution to the costly and slow nature of traditional international payments.

• Speed and Availability: Stablecoins facilitate near-instant, 24/7, non-intermediated transactions, which is especially relevant for cross-border transfers that typically take multiple days and demand high fees.

• Financial Inclusion: In economies facing high inflation, currency devaluation, or limited banking access, stablecoins pegged to stable fiat currencies (like the USD) serve as a trusted safe asset and a vital payment rail. Over 40% of stablecoin users in emerging economies rely on them for daily transactions.

2.2. Institutional and corporate use

For large enterprises, stablecoins solve pain points in liquidity management and settlement:

• Treasury Management: They enable instant transfers of liquidity across accounts and entities, automating cash sweeps and internal settlements, reducing reliance on overnight batch processing. Companies like Ferrari and SpaceX are using stablecoins for cash management.

• Tokenized Financial Markets: Stablecoins play a key role in tokenization, allowing for the real-time settlement of securities (Delivery-versus-Payment, DvP) or cross-currency swaps (Payment-versus-Payment, PvP), potentially increasing liquidity and transparency while reducing counterparty risk.

2.3 Vehicle for digital markets and DeFi

The most recognized use case is their function as a “vehicle currency” on crypto exchanges, serving as a liquid bridge between volatile crypto assets and fiat currencies. Furthermore, stablecoins are essential building blocks for Decentralized Finance (DeFi) protocols, underpinning services such as collateralized lending and asset management.

3. The stability paradox: Risks and vulnerabilities

Despite their name, stablecoins are not immune to volatility. While less volatile than Bitcoin, they are typically more volatile than traditional assets like gold or the US dollar. Their reliance on collateral and market mechanisms introduces several inherent risks.

3.1 The risk of runs and peg failure

Stablecoins are acutely vulnerable to sudden redemptions, known as a ‘stablecoin run,’ where holders rush to convert their coins back into fiat currency.

• Algorithmic vulnerabilities: Algorithmic stablecoins have proven highly fragile, with collapses like TerraUSD demonstrating the intrinsic flaws in non-collateralized designs.

• Contagion from traditional banking: Even stablecoins backed by high-quality reserves are exposed to banking system shocks. For example, USDC temporarily de-pegged in March 2023 following the collapse of Silicon Valley Bank (SVB), where $3.3 billion of its reserves were held. This revealed a vulnerability to concentrated traditional finance exposure.

• Reserve quality and opacity: The business model of issuers involves capturing “seigniorage” (interest earned on reserve assets). This creates a strong incentive for issuers to invest in higher-return, potentially less liquid assets. If the reserves are risky or opaque, stablecoins are vulnerable to self-fulfilling runs.

3.2. Systemic financial risks

The proliferation of stablecoins raises concerns for overall financial stability.

• Asset fire sales: Since major stablecoin issuers (like Tether and Circle) are already significant holders of US Treasuries, a mass redemption event could force them to liquidate these vast reserve holdings rapidly. This “fire sale” could drive down bond prices, increase interest rates, and trigger broader financial market turmoil.

• Lack of safeguards: Stablecoins lack traditional safeguards such as FDIC deposit insurance or a guaranteed lender of last resort (like a central bank). Taxpayers could ultimately be implicated in bailing out failed stablecoins if stability concerns escalate.

• Financial crime and compliance: Stablecoins are attractive tools for anonymous and illegal transactions (e.g., circumvention of capital controls, money laundering, and sanction evasion). Current KYC/AML compliance enforcement varies widely across jurisdictions, posing significant challenges to regulators.

4. Stablecoins and the future of banking

The widespread adoption of stablecoins could significantly impact the existing banking system, particularly concerning deposit funding and credit intermediation.

4.1. The threat of deposit disintermediation

Financial institutions historically rely on deposits for healthy margins and credit activity. If consumers and corporations widely migrate deposits into stablecoins, banks face two main challenges:

1. Funding competition: Banks could lose low-cost deposits, forcing them to increase deposit interest rates (negatively impacting margins) or rely on more expensive, non-deposit funding sources.

2. Credit contraction: A sufficient shift of deposits to stablecoins could reshape the banking sector’s funding mix, potentially leading to a higher overall cost of credit intermediation in the economy.

However, some experts argue that this risk may be overstated in the near term, believing that any significant migration would require stablecoins to offer better economics or lower payment friction than traditional bank deposits. Moreover, banks offer a comprehensive suite of services (insured deposits, fraud protection) that stablecoins cannot easily replicate.

4.2. Stablecoin architecture and credit provision

The macroeconomic impact on credit depends heavily on the stablecoin’s reserve structure:

• Bank-based stablecoins (unsafe by design): If stablecoin issuers collateralize their coins primarily with bank deposits (as suggested by certain regulations like the EU’s MiCA framework for “significant” stablecoins), they create a direct, dangerous link between stablecoins and banks. While this structure would maintain the traditional credit creation role of commercial banks (since the reserves remain deposits in the system), it leads to a “doom-loop” where a run on the stablecoin directly creates risks for the underlying banks.

• Bond-based stablecoins (narrow bank model): Stablecoins backed primarily by short-term government bonds (Treasuries) are considered safer by design. If these issuers were regulated as narrow banks, they would minimize run risk but could potentially reduce credit intermediation by shifting funds away from lending capacity. However, bond-based stablecoins have the potential to create money by purchasing government bonds.

4.3. Geopolitical and monetary policy implications

Since almost all stablecoins are pegged to the US dollar, their global proliferation has geopolitical implications.

• Strengthening the US dollar: Widespread international use of dollar-denominated stablecoins could indirectly finance US government debt and increase global demand for the dollar, reinforcing the “exorbitant privilege” of the US dollar.

• Monetary sovereignty: Conversely, if populations in countries with weak domestic currencies shift massively to stablecoins, it could drain local deposits, undermine the effectiveness of local central banks to conduct monetary policy, and lead to de facto “dollarization”.

4.4. Regulatory imperative

Recognizing these systemic risks, regulatory frameworks are rapidly evolving globally.

• The markets in crypto-assets (MiCA) framework in the European Union strengthens disclosure and governance requirements.

• The recently passed US GENIUS Act creates the first federal supervisory system, aiming to drive mass adoption by requiring stablecoins to be backed 1:1 by high-quality, liquid assets (like Treasuries and deposits) and subjecting issuers to bank-like regulation. This oversight is intended to create a sense of safety and drive mainstream trust.

Final thoughts: Navigating the next wave

Stablecoins represent a genuine inflection point in global finance. While they promise revolutionary improvements in cross-border payments, treasury management, and DeFi, they concurrently challenge core tenets of financial stability, monetary policy, and the traditional banking model.

For financial institutions, the opportunity is urgent: engage now to decide where to play—whether through issuance, custody, on-ramping, or integrating stablecoins into existing treasury and payment offerings—rather than waiting for technical issues to be fully resolved. Forward-looking policy and institutional engagement are crucial to ensure that this technological breakthrough leads to a more efficient and resilient financial system, rather than an era of “economic chaos”.

----------------------

References

Arner, D., Auer, R., & Frost, J. (2020). Stablecoins: risks, potential and regulation. Financial Stability Review, Issue 39, Banco de España.

Bofinger, P. (2025). Stablecoins and the Future of Money: Economic Principles and Policy Implications. IMK Study, No. 100.

Boston Consulting Group (BCG) (2025). Stablecoins: Five Killer Tests to Gauge Their Potential.

Briola, A., Vidal-Tomás, D., Wang, Y., & Aste, T. (2023). Anatomy of a Stablecoin’s failure: The Terra-Luna case. Finance Research Letters, 51, 103358.

Goldman Sachs (2025). Stablecoin Summer: Top of Mind.

Liao, G. Y., & Caramichael, J. (2022). Stablecoins: Growth Potential and Impact on Banking. International Finance Discussion Papers 1334. Washington: Board of Governors of the Federal Reserve System.

Moura de Carvalho, R., Coelho Inácio, H., & Figueiredo Marques, R. P. (2025). From instability to regulation: A systematic literature review on stablecoins. The International Journal of Digital Accounting Research, 25, 71–101.

Mitsu Adachi, P. B. P. S., Alexandra Born, M. C., Stephanie Czák-Ludwig, Isabella Gschossmann, A. P., S.-M. P., Mirjam Plooij, I. R., & Pierfrancesco Zeoli (2022). Stablecoins’ role in crypto and beyond: functions, risks and policy. Macroprudential Bulletin 18, European Central Bank.

----------------------

Disclaimer

The views and opinions expressed in this article are solely those of the author(s) and do not reflect the views, policies, or positions of their employer or any other entity.